Aligning your purchasing and supply chain management with the aims and objectives of your members and your organisation

Yes, this is a topic about financial management and control, therefore it’s bound to be boring, unexciting and dull. Just flick over and ignore it, it’s fine…or is it?

It is my experience that associations overlook the many benefits that strategic financial management can bring to organisations: they focus on routine reporting of income and expenditure with little investment in strategic finance delivery. The distinct advantage an association gains when a finance function is connected and fully understands the growth objectives and value that members receive generally repays the investment many times over.

Just think about it for a moment and reflect upon what goes on inside your organisation. Is your spending controlled? Do you have a robust governance framework surrounding purchasing and supply? Is the culture of your organisation a bit like the wild west or is it so wound up in bureaucracy that nothing ever changes? Have you outsourced it to an Association Management Company or Event Management Company and as a consequence relinquished spending power and control?

Or how about this: does your association align its purchasing and supply chain management with the value proposition you put towards retaining members and attracting new ones to continually grow your organisation? In other words: can associations be smart, connected and rational when it comes to strategy and buying decisions?

Buy smarter, buy together & be rational

The focus of this article is to provide a few pointers so that associations can develop plans and begin to implement a strategy to maximise the value of transactions with suppliers and reduce waste. It is the topic I covered at the Associations World Congress in Berlin.

We will look at how the executive or board can influence and effect a rational buying strategy through management techniques and data analysis so that the spend culture of an organisation is pointed in a focused direction and visibly governed and wholly supported by a connected and commercially aware finance function so it can become the business partner to the organisation rather than just the accounting department. This starts with the concept of Buy Smarter, Buy Together, Be Rational.

Buy smarter

Generally when you see the word Smart or Smarter in management speak you tend to think of its use as an acronym [Specific, Measurable, Achievable, Realistic and Time Bound]. Whilst this has its uses, and when used, normally involves sitting through a presentation and fearing death by PowerPoint; for the purpose of it right now, the word is just its plain meaning:

Smart

This is all about having smart reporting available and this means utilising the data held in your accounting system to do more than solely report income and expenditure. You can structure your systems to record costs so that you are able to analyse supplier performance & spend behaviours and come up with a scheme of segmenting suppliers & analysing spend categories in a way to focus on and scrutinise spending patterns, supplier choices and procurement decisions.

Buy together

This focusses on creating a culture of unity to achieve smarter buying. It means setting up a framework of oversight & control and always ensuring that support is available from key people in your organisation to those that are making buying decisions.

Be rational

This is probably the most important but the most difficult of the three concepts to achieve; it means setting defined and measureable objectives before major spending decisions. Ensuring that spend is always in line with the objectives and growth ambitions of your association. And finally, ensuring that you utilise the smart data to analyse and evaluate spending decisions before and after the spending event, and then allowing this data to influence decision making for now and the future. Above all, this is a culture that everyone who purchases and plans within your organisation can buy into.

First things first

So that’s the concept, what’s the objective? The objective is to focus spend on those activities that generate the most value for your membership body, in other words, minimise or eliminate spend on low-value, low-risk activities and maximise the available budget on high-value derived activities.

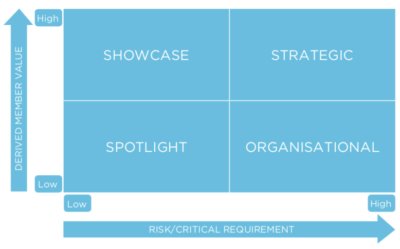

The Value and Risk Matrix

The simple matrix displayed is a useful tool to drive focus and begin to scrutinise your association’s spending behaviours and whether or not they are aligned with the overall objectives & strategy of your association. The matrix is split into four sections on two axes of high and low. These are: derived member value and risk or critical requirement.

The membership body derives value from the organisation’s activities, amongst others, through events, publications, use of its knowledge base, links & networking with other members. You are able to assess, by listening to and recording data from the membership community about the value of activities on offer. Some activities are essential, some are strategic, and some are non-essential but they are adding value to the membership body. There will be some activities that derive little or no value to the membership body and carry a minimum risk to your organisation if the activities cease.

The first question to focus on is asking: What value does your membership body and connected stakeholders value from your activities? If you can answer this, then you can begin to put your plans into action. If you ask the right questions to your membership body you can begin to segment & categorise. To do that you must measure the value and risk of those activities going on within your association, to your association.

Suggested objective

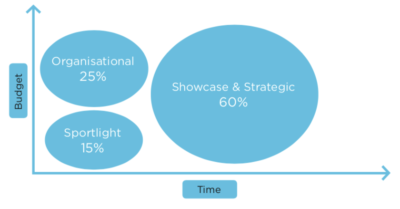

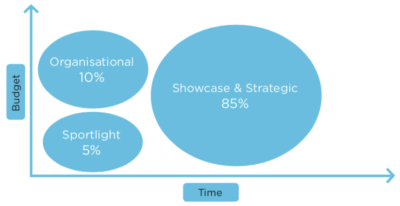

The charts displayed are a good example of what the objective of employing a strategy like this. The focus is on spending or investing for growth.

We want to go from this:

To this:

How do you begin to implement such a strategy?

Assuming that it is a core objective to achieve membership body growth, this is a tool that can be used for analysis of spend within your organisation so that you can picture to what degree your spend is aligned with your organisational plans.

The ultimate aim is that for any given purchase or spending decision, you can critically assess the value of it to your organisation and categorise it.

The leadership & executive function can take ownership of this tool to derive sound spending principles and policies that can be followed throughout the organisation. Those principles and policies can be defined for each quadrant so that the spending by the organisation can start or become more focused on creating member value.

It is also recommended to have major activities of your association analysed by this matrix. For example, analyse your budget for your congress or annual meeting using these techniques; you can drilldown, the technique does not just have to be for your overall organisation.

The following is an example of how to interpret the categories and therefore understand the value and risk relationship within your organisation.

Showcase

These purchases and services appeal highly to the member body but may not be deemed absolutely necessary by the organisation. These services derive high satisfaction from the member body and are therefore important and can serve as tools for membership growth. A good example can be a high-quality website and associated social media connections. A website, Twitter account and Facebook account may be able to be run using basic free tools available on-line but an investment in this area can connect them all together and appeal highly to current and prospective members.

Strategic

These purchases are the most important ones in your organisation. They represent high value for the membership body and a high degree of risk to the organisation. Without these, membership numbers would decline sharply and therefore finances would deteriorate. A typical example would be the essential elements of an annual meeting or congress.

Organisational

Items appearing here are necessary purchases that underlie and support the structure of the organisation. It is the types of services that are not noticed until they are missing. They derive low value from the membership body and are those services traditionally seen as bureaucratic and administrative but critical. A typical example would be insurance or legal services, or dare I say accounting services, but I’m arguing for them to appear in the strategic section.

Spotlight

Anything that appears in this quadrant needs to have a “light shined” on it. An assessment of why the organisation is spending anything in this quadrant is required. It is here where it is highly likely to be able to identify waste or unnecessary spend. All items appearing here should be challenged.

How to use it!

A tool such as the one described above can effect and improve the governance and culture of spending throughout the whole organisation. Such a focus can have a significant impact on the financial position of an organisation. It’s not about spending less, it’s about spending better in advancement of your organisations objectives and purchasing procedures & policies need to be structured to support the focused strategy.

Your accounting systems and chart of accounts can be set up in a way to extract key and meaningful management information about your organisation’s spending patterns and behaviours. It probably means being able to have three levels of analysis available in your accounting system: account, cost centre and segment. This is surprisingly easy to do and most accounting packages can cope with it, but what it does need is some thought and planning.

It is vital that the leadership function takes ownership of the organisations spending and uses rational-based strategies to pursue improvements to spending principles and policies. Regular reviews at leadership and regular refreshing of categorisations can influence the spend culture of the organisation.

Here’s a suggestion for a starting point to define principles and ultimately policies towards spending in your association.

The above enhancement to the matrix suggests simple strategies to apply for each quadrant, with a focus on how to measure the importance of value-for-money, quality and price and where to place it in a plan of priorities.

Showcase spending strategy

Cost items for activities finding their way into the showcase section appeal highly to the membership community and connected stakeholders; these activities are likely to drive growth and increase member numbers. Therefore, the overall focus should be value-for-money. Suggested approaches include:

- Introducing competitiveness in the bidding and tender process with a focus on quality and price.

- Look to transform cost into a revenue stream (sponsorship, premium services).

- Fully understand what it is about this service that members value.

- Routinely request feedback from the membership base to ensure that these services are still valued - trends change quickly (remember QR codes).

- Eliminate spend showing a decline in perceived member value - act now before it becomes a burden.

- Supply should be expert-led, you want a high quality finish.

Strategic spending strategy

Cost items for activities finding their way into the strategic section represent the most important ones in your organisation: they are high value to your members and high risk to your organisation. If these are not present, then your member numbers start to reduce, commercial partners lose interest and income falls.

- Spend in this category tends to be for infrastructure and investments (website building, critical event costs, flagship publishment).

- All spend should be project-based.

- All projects should have a project sponsor at board level.

- All projects should have a project manager (outsourced or internal).

- Project objectives must be S.M.A.R.T.

- Outcome should be measurable by return on investment against original investment case.

- Suppliers should be selected on the basis of their ability to partner with the organisation.

Organisational spending strategy

Cost items for activities finding their way into the organisational section are those your members don’t really value, but these are critical to your organisation: legal requirements, statutory requirements and essential administration and governance. Without these you could not run your organisation:

- Introduce competitiveness in the bidding and tender process and ensure a thorough approach to contract management.

- Incentivise incumbents to agree contract efficiencies.

- Review section regularly to relegate spend to spotlight category.

- Contracts tend to be over a pre-determined period of 12 months or over (insurance, secretariat, bookkeeping). Set targets to reduce costs per paying member with incumbent suppliers by benefiting from a learning curve effect.

- Routinely go to the market on individual services and occasionally get another supplier to do a one-off job for you to ensure minimal complacency from incumbents.

- Analyse cost-effectiveness and the reduction of proportion of spend by measuring cost per member on a regular basis in line with the contract term.

- Benchmark prices and share knowledge within the association community.

Spotlight spending strategy

Cost items for activities finding their way into the Spotlight section need to be robustly challenged. It’s these items that derive low value and are low risk to the organisation. The overall strategy here must be to eliminate the cost occurring here.

- Target waste and identify savings.

- Reduce budgets and challenge long-held preconceptions.

- Increase oversight.

- Demand evidence-based justification (promote spend using rational buying techniques).

- Spend must be for the least possible price and the choice of supplier is not as important.

- Signed off spend in this category needs to be highly visible and therefore board members are easily made aware of spending in this category.

Closing summary

The Value & Risk matrix is an example of employing a simple tool to transform the spending culture of an organisation, and it can be truly transformational. Remember: the objective is not to spend less but to spend better and towards the advancement of your organisations objectives, mission and member body growth.

It is becoming increasingly important for the finance function of an association to be more than just the accounting department and take a strategic lead and be fully connected to the organisation’s growth ambitions and strategy. Leadership teams, executive boards and associated stakeholders are also demanding more commercial savviness from their finance function. But a lot of the time, they lack the tools and the structures to develop a rock solid foundation to build the strategy on and fully realise the benefits. In terms of systems and structures, all it takes is a few simple changes, but the real challenge comes when addressing culture and getting buy in at every level.

If you can overcome these challenges, then you will find that your membership body becomes more satisfied with the output from activities, your suppliers are kept to the top of their game by becoming more accountable and your financial position would likely be strengthened.